What Is GAP Insurance, and Do You Actually Need It When Buying a Car?

GAP insurance can be worth it if you finance (or lease) a vehicle and could owe more than the car is worth during the first few years of ownership.

If you’re shopping for a used car in Lufkin, Texas, GAP coverage is one of the most common “do I really need this?” add-ons buyers ask about. The short version is simple: it protects you from a very specific money problem after a total loss.

Below is a clear, practical breakdown of what GAP coverage is, why it matters, and how to decide if it makes sense for your purchase.

Quick definition of GAP insurance

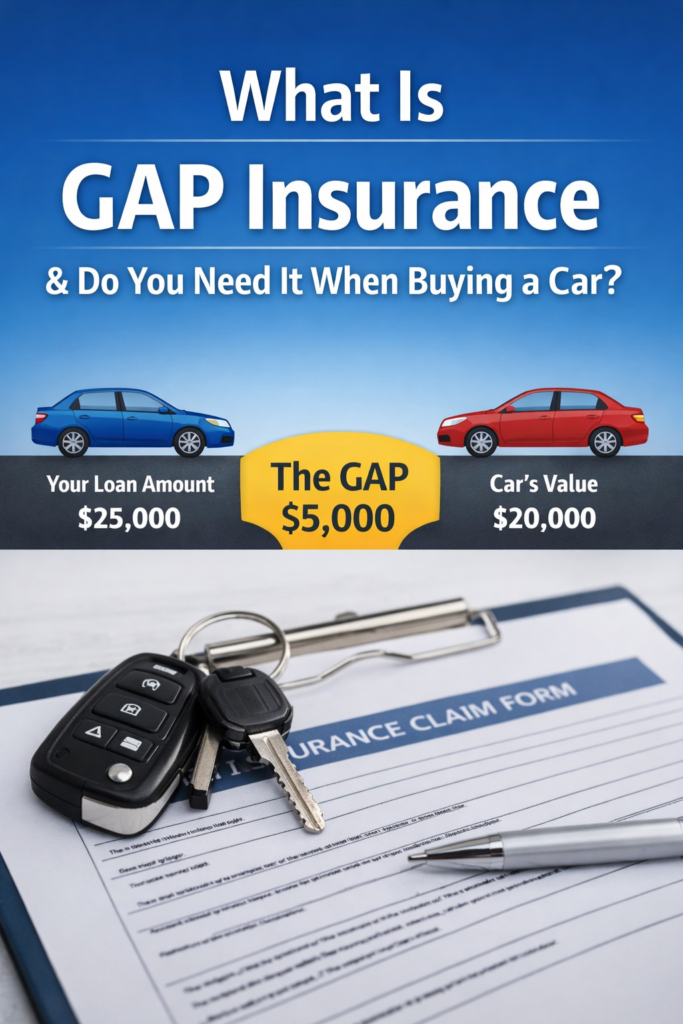

GAP insurance (Guaranteed Asset Protection) helps pay the difference between your vehicle’s actual cash value (what your insurer says it’s worth) and what you still owe on your auto loan or lease if the car is totaled or stolen.

GAP insurance at a glance

| Topic | Plain-English answer |

| What it protects | The “gap” between your loan/lease payoff and your insurance settlement after a total loss |

| When it applies | Typically, after theft or a totaled vehicle claim (when comprehensive/collision pays ACV) |

| Who it’s for | Buyers with small down payments, long loan terms, or rolled-in negative equity |

| Who can skip it | Buyers with large down payments, short terms, or who owe less than the car is worth |

| Is it required in Texas? | Not by law, but some lenders/leases may require it |

What GAP coverage is (and what it isn’t)

GAP coverage is not “extra car insurance” that pays for repairs or upgrades. It’s a loan/lease protection product that kicks in when your regular insurance payout isn’t enough to clear what you still owe.

This situation is more common than most people think because vehicles depreciate quickly, especially early on. If you total the car before your loan balance drops below the car’s value, you can be stuck paying the leftover balance out of pocket.

GAP insurance vs. “full coverage”

A lot of buyers assume “full coverage” means they’re fully protected from any financial hit. In reality, comprehensive and collision generally pay the vehicle’s actual cash value (ACV), not the amount you owe.

That’s why GAP exists: it addresses the difference between ACV and the loan/lease payoff when there’s a shortfall.

How GAP insurance works in a total-loss claim

Here’s the typical flow, step by step.

- You have a covered total loss (accident, theft, etc.) and file a claim with your auto insurer.

- Your insurer determines the vehicle’s ACV right before the loss and pays that amount (minus your deductible).

- Your lender calculates the payoff amount on your loan or lease.

- If the payoff is higher than the insurance settlement, GAP coverage may pay the difference (based on the contract terms).

A simple GAP example

Let’s say you’re driving around Lufkin and your vehicle is totaled.

| Item | Amount |

| Loan payoff balance | $22,500 |

| Insurance settlement (ACV) | $19,000 |

| Deductible | $1,000 |

| Remaining shortfall | $4,500 |

Depending on the contract, GAP may cover some or all of that shortfall (often after the primary insurance payout), which can prevent you from writing a painful check to the lender.

What GAP insurance usually covers (and doesn’t)

Coverage details vary, but most GAP products are designed to cover the core gap: loan/lease balance minus ACV settlement.

| Usually covered | Often not covered (or limited) |

| The payoff shortfall after a total loss | Overdue payments, late fees, or penalties |

| Total loss from theft (when comprehensive applies) | Extended warranties, service contracts, routine maintenance |

| Sometimes a portion of your deductible (depends on plan) | Modifications, accessories not included in ACV |

| Sometimes a capped amount or percentage limit (plan-specific) | Amounts beyond contract limits or excluded scenarios |

The key takeaway: GAP is narrow by design. It’s meant to protect your loan balance, not replace your main auto insurance.

Why GAP insurance matters for many used-car buyers

GAP is often discussed as if it’s only for brand-new cars, but used buyers can still benefit. It comes down to how your loan is structured, not just the model year.

GAP can matter more when you have any of the following:

- A low down payment (or $0 down)

- A longer-term loan (60–84 months)

- A higher interest rate

- Negative equity rolled into the new loan (you owed on the trade)

- A vehicle that depreciates faster than average

Even on a used vehicle, these factors can keep your loan balance higher than the car’s value for a while.

Do you need GAP insurance? Use this decision table

This is the quickest way to self-check.

| Your situation | GAP insurance is usually… | Why |

| You put little to no money down | A smart idea | You’re more likely to owe more than the car is worth early on |

| You financed for 72–84 months | A smart idea | Depreciation can outpace payoff for longer |

| You rolled negative equity into the loan | Strongly recommended | You’re starting “upside down.” |

| You made a large down payment (20%+) | Often optional | You may avoid being upside down from day one |

| You financed for 36–48 months | Often optional | Balance drops faster |

| You could easily pay the gap out of pocket | Optional | GAP mainly protects cash flow in a worst-case event |

| You’re paying cash | Not needed | There’s no loan balance to protect |

If you want one rule of thumb: if the car could be totaled tomorrow and you’d still owe more than the insurance payout, GAP is doing a real job.

Is GAP insurance required in Texas?

Texas rules require lenders to disclose that a borrower is not required to purchase a GAP waiver agreement to obtain the loan.

However, lenders and leasing companies sometimes require it as a condition of financing, especially when risk is higher (like low down payments).

Where to get GAP coverage

Most buyers see GAP offered in one of three places:

1. Through the dealership or lender

This is common because it’s easy to bundle into your monthly payment. It can also be convenient because it’s tied directly to the loan.

The downside is that rolling it into the loan means you may pay interest on it, and cancellation rules can vary by contract.

2. Through your auto insurance company (loan/lease payoff coverage)

Many insurers offer something similar, often called “loan/lease payoff.” Some versions require you to carry comprehensive and collision to add it.

This can be cost-effective, but it may have payout caps, so it’s important to compare the maximum benefit against your potential gap.

3. Through specialty providers

Less common for everyday buyers, and the details vary widely. If you go this route, focus on exclusions, claim process, and maximum payout.

How long should you keep GAP insurance?

Most people only need GAP while they’re at risk of being upside down.

A simple approach is to review your loan balance and your vehicle’s approximate market value at least once a year. Once you owe less than the car is worth (or close enough that you’re comfortable covering the difference), you can usually drop it.

Smart questions to ask before you buy GAP

Bring these up before you sign, and you’ll avoid most surprises.

- What is the maximum payout limit?

- Does it cover my deductible, and if so, how much?

- Are there exclusions (late payments, certain uses, modifications)?

- Can I cancel it, and do I receive a refund if I do?

- If it’s rolled into the loan, how much interest will I pay on it over time?

These questions also make it easier to compare dealership GAP vs. insurer loan/lease payoff coverage.

How Raceway Motors Can Help

If you’re financing a vehicle and want help choosing the right protection for your budget, the team at Raceway Motors in Lufkin can walk you through your options and keep it simple. Start by browsing our current selection, and if you’d like to see your buying power first, you can apply today.

Frequently Asked Questions About GAP Insurance

Does GAP insurance cover theft?

Yes, GAP can apply if your vehicle is stolen and your comprehensive insurance pays a total-loss settlement, but the settlement still doesn’t cover the loan or lease payoff.

Do I need GAP insurance on a used car?

Sometimes, yes. If you financed with a small down payment, long term, or rolled negative equity into the deal, you can still be upside down on a used vehicle, which is exactly what GAP is designed for.

Do I need GAP insurance if I have “full coverage”?

You might. “Full coverage” (comprehensive and collision) generally pays ACV, not what you owe, so you can still have a shortfall if you’re upside down.

Can I buy GAP insurance after I purchase the car?

Sometimes, depending on the provider and your loan details. Many dealership/lender plans are easiest to add at purchase, while insurer loan/lease payoff options may be available when you start or adjust your auto policy.

When is GAP insurance usually not worth it?

It’s often not necessary if you put a large down payment down, have a short loan term, or you owe less than the car is worth. It also isn’t needed if you’re paying cash.

Is GAP insurance required in Texas?

Not by law, but it may be required by your lender or lease agreement, depending on the deal.